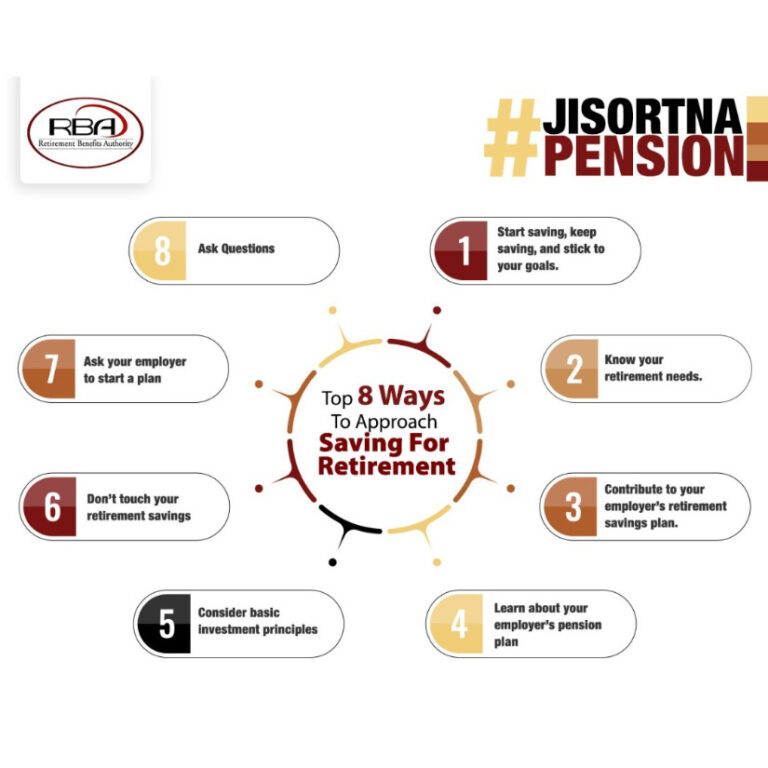

1) Start saving, keep saving and stick to your goals.

If you are already saving, whether for retirement or another goal, keep going. If you’re not saving, it’s time to get started. Start small if you have to and try to increase the amount you save each month. The sooner you start saving, the more time your money has to grow. Make saving for retirement a priority. Devise a plan, stick to it, and set goals. Remember, it’s never too early or too late to start saving.

2) Know your retirement needs.

Retirement is expensive. Experts estimate that you will need 70 to 90 % of your pre-retirement income to maintain your standard of living when you stop working. Take charge of your financial future.

3) Contribute to your employer’s retirement savings plan.

If your employer offers a retirement savings plan, sign up and contribute all you can. Find out how much you would need to contribute to get the full employer contribution and how long would you need to stay in the plan to get that money.

4) Learn about your employer’s pension plan

If your employer has a traditional pension plan, check to see if you are covered by the plan and understand how it works. Ask for an individual benefits statement to see what your benefit is worth. Before you change jobs, find out what will happen to your pension benefit. Learn what benefits you may have from a previous employer.

5) Consider basic investment principles

How you save can be as important as how much you save. Inflation and the type of investments you make play important roles in how much you’ll have saved at retirement. Know how your savings or pension plan is invested. Learn about your plan’s investment options and ask questions. Put your savings in different types of investments. By diversifying this way, you are more likely to reduce risk and improve return.

6) Don’t touch your retirement savings

If you withdraw your retirement savings now, you’ll lose principal and interest and you may lose benefits or have to pay withdrawal penalties. If you change jobs, leave your savings invested in your current retirement plan, or roll them over to your new employer’s plan.